The recent sale of NFTs from Yuga Labs showed both the promise and the peril of the hyped technology. On the one hand, Yuga Labs made “$320 million in what was considered the “largest NFT mint in history”, with its “sale of Otherdeed nonfungible tokens that represent digital land deeds on their new venture, the Otherside metaverse”.

Minting is the NFT equivalent of an “initial public offering” (IPO). But instead of selling stock, they are selling a digital token. In this case it was land rights in “a metaverse game world”. Each parcel of “digital land” was sold for “305 ApeCoin (APE), or nearly $5,800”. The incentive for the buyer is to get in early and then sell the NFT on secondary markets. For example, on OpenSea (a major reseller of NFTs) the Otherdeeds were selling for an average of just over 9 ether (ETH) or nearly $27,000.

The peril?

The rush to cash in on this craze resulted in overloading the Ethereum blockchain. And that didn’t just result in slow service. It cost millions: $123 million. Users got hit with transaction costs that exceeded the cost of the “digital land deed”, coming in between “2.6 ETH ($6,500) to 5 ETH ($14,000)”.

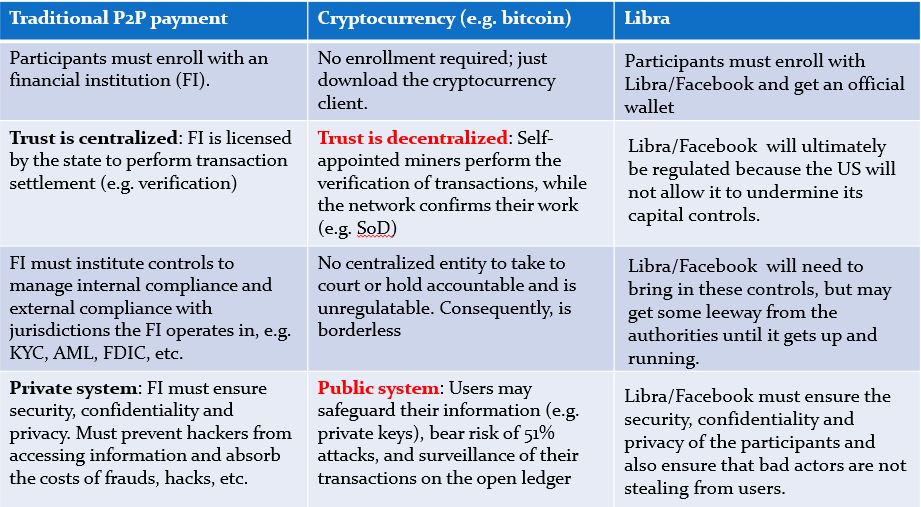

In contrast, Visa charges merchants between “2.87 percent and 4.35 percent per transaction”, which would have been about $160-$260 per sale. It’s hard to see how the decentralized finance (DeFi) approach is superior to the “classic” approach of centralized finance (CeFi).

So, should we discard NFTs?

NFTs: What took them to the Peak of Inflated Expectations?

Before running for the hills and closing the books on NFTs, we should remember the Dotcom era. It was the late 1990s, Google was still a scrappy start-up and Microsoft was seen as the bully those days. And people will all starry eyed about the “new Internet economy’. Slap a “.com” behind your company’s name and voila! Millions of dollars of investment would be thrown at you.

So, is history repeating itself? In a sense, yes.

According to Gartner’s Hype Cycle, there is an initial hype phase when the innovation causes mania in the markets, which is known as the “Peak of Inflated Expectations”. That is, the innovation is seen as that silver bullet that will cure all.

Conceptually, NFTs provide a means to create “digital scarcity”, hence the term “non-fungible”. Specifically:

“NFTs allow ownership and use rights to be demonstrated for any piece of digital content by assigning the content a specific, nonduplicable identifier that is recorded on a distributed database, or blockchain, typically Flow or Ethereum.” (link)

This then allows physical collectible items – basketball cards, comic books, art, and so on – to be unique digital items. Previously, this was not possible as all digital “assets” were fungible, i.e. copies of copies with no way to distinguish one from another.

A secondary area of value within NFTs is the use of algorithms to generate art. Specifically, algorithms are used to synthesize “different design features, accessories, and special traits… [to create] thousands of unique combinations.” In other words, an artist does not have to generate each work of art. Instead, they can “draw” one piece and then let the algorithm generate thousands of images based on that initial design. For example, the “Ape images” generated as part of the Bored Ape Yacht Club “collection” relied on this “procedural algorithms that can create tiers of rarity and value”.

Beyond art, sports media looks to be a potentially lucrative NFT market. Deloitte Global predicts between 4 to 5 million gifts/purchases for such digital work that “will generate more than US$2 billion in transactions in 2022”.

Entering the Trough of Disillusionment: 10 Challenges with NFTs

The value of NFTs is intuitive at first glance. But there are challenges. The emergence of these problems, issues, and outright scams is a sign that we are heading into the next phase of Gartner’s Hype Cycle which is “the Trough of Disillusionment”. If this was the early days of the Internet, it would be the moment when investors realized that pets.com was not such a good idea after all. It’s in this phase that the problems with the innovation become apparent. Let’s look at 10 issues that have arisen with NFTs.

Issue #1: Blockchain does not scale like the Cloud

The +$100 million gas bill that Ethereum effectively issued to “digital land deed” speculators was not a first. This problem was previously experienced with CryptoKitties. As noted in this paper, “CryptoKitties was the first widely recognized blockchain game. Players could own, breed, and trade kitties, which are the only prop in the game.” The paper explains how collectors experienced massive gas bills from Ethereum to get in on the hype:

“The cost of performing operations on a public blockchain system is highly volatile due to the unstable price of cryptocurrencies, resulting in it difficult to control the cost of the applications deployed on the blockchain. As CryptoKitties was deployed on Ethereum, the cost of playing the game (including the costs of buying, breeding, and renting kitties, as well as the fees paid to Ethereum miners) has risen significantly due to the rapid rise of Ether price in the third stage. Ether price increased from US $451 on December 10, 2017, to US $1,322 on January 10, 2018…resulting in a significant increase in the cost of playing the game, raising the bars for new players entering the game.” [Emphasis added]

We’ve been conditioned by the cloud to expect automatic scaling; such bottlenecks seem to harken back to a more primitive era of computing. However, that’s the price of trust. The proof-of-work consensus mechanism is designed precisely to slow things down to allow for the miners to verify the transactions and prevent hackers from committing non-authorized records to the blockchain.

Issue #2: NFTs do not necessarily convey digital ownership

According to Deloitte Global: “Ownership of an NFT may include ownership of the underlying digital asset, though most sports NFTs sold to date have no ownership or use rights in the underlying media.” [Emphasis added, italics from original]

But perhaps a bigger smoking gun is at Christie’s auction house – the same one that sold Beeple’s digital artwork for $69 million. As highlighted by the well-known nocoiner, David Gerard: “Christie’s auction of an NFT is a fabulous worked example. There’s a 33-page terms and conditions document, and if you wade through the circuitous verbiage, it finally admits that … you’re just buying the crypto-token itself…”

He goes on to cite the terms of sale, right from the Christie’s site, which clearly states:

“You acknowledge that ownership of an NFT carries no rights, express or implied, other than property rights for the lot (specifically, digital artwork tokenized by the NFT)…”

Issue #3: If all that’s transferred is a hash, then where’s my “digital asset”?

The “what” is not the only issue. The ”where” is also an issue. As noted on CoinDesk: “On the simplest level, an NFT is a record (a document with a hash) stored on Ethereum (usually) that points to where its associated content (the image) lives somewhere else on the internet (it's much too expensive to store images on Ethereum).” [Emphasis added]

Like scalability, we are accustomed to the idea that storage is cheap and plentiful. But such assumptions don’t hold for the blockchain. Therefore, this disconnect between the location of the ownership record and the digital item itself can be baffling. Moreover, this approach contradicts that generally accepted wisdom that ‘possession is nine-tenths of the law’.

Issue #4: Is digital art a great vehicle for money laundering?

As noted by the US Department of the Treasury: “…the emerging digital art market, such as the use of non-fungible tokens (NFTs), may present new risks, depending on the structure and market incentives.”

Though specifics were not provided, it’s not surprising the that the US government has their eye on the area. Given the reputation that Bitcoin has for us in less than legal transactions, it’s not surprising that NFTs potential for nefarious purposes.

Issue #5: NFT Price Volatility is an Understatement

One of the more famous NFTs was Jack Dorsey’s first tweet, which was sold for $2.9 million. According to the Guardian, Sina Estavi, a crypto entrepreneur, who bought the tweet wanted a cool $48 million for it. What was he offered? According to CBS, only $280.

Issue #6: You could be buying an NFT that has been copied without the author’s permission

OpenSea noted in a tweet that “Over 80% of the items created with this tool were plagiarized works, fake collections, and spam.” Perhaps, the worst incident of this was how fraudsters sold the work of a dead artist. Moreover, “NFTs themselves can be used to fraudulently attribute digital designs to multiple owners”.

Issue #7: The superstar NFT artists make all the money, the rest of us don’t

The hype would make us believe that we all can get rich from NFTs. A study published on Nature found that 75% of NFTs sold for a price less than $15:

“We observe that the average sale price of NFTs is lower than 15 dollars for 75% of the assets, and larger than 1594 dollars, for 1% of the assets. Considering individual categories, NFTs categorized as Art, Metaverse, and Utility reached higher prices compared to other categories, with the top 1% of assets having average sale price higher than 6290, 9485, and 12,756 dollars respectively.”

Issue #8: For all the promise of blockchain’s transparency, opaqueness abounds

As noted earlier, digital artist Beeple (Mike Winkelmann) sold his "Everydays - The First 5000 Days" for $69 million. But the buyer was a mystery. But nocoiner Amy Castor had a hunch. She thought it was MetaKovan (Vignesh Sundaresan). And this was confirmed on CNBC.

But so what? It turns out that MetaKovan and Beeple were already business partners.

Beeple owns 2% of the B20 tokens that is behind Metapurse “a crypto-based investment firm”. Metapurse is controlled by MetaKovan. That firm had previously purchased “Beeple’s “Everydays: 20 Collection” artworks for $2.2 million”. (See Castor’s post here). Though the "Everydays - The First 5000 Days” is owned by MetaKovan and not Metapurse, the previous relationship does dampen the hype behind the sale and calls to us to question the valuation.

But a more important question, is why wasn’t this visible on the Ethereum blockchain? According to Castor:“…it sounds like the funds may even have gone into Christie’s escrow wallet…Anyhow, if both parties had Coinbase accounts, the exchange could just change the database records off-chain to flip account balances. In this way, Coinbase acts like a second layer, and you wouldn’t see the ETH transaction.” [Emphasis added]

Issue 9: NFTs still rely on “classic” intermediaries for mega sales

NFTs that sell the best still rely on “old-world” forms of intermediaries. That is, NFTs are not a way for the “common person” to make it rich simply because of their artistic talent. Instead, the more successful NFTs rely on the following:

· Celebrity endorsements: Paris Hilton, Jimmy Fallon, Eminem, and others used their celebrity status to give a boost to the NFT “Ape Art” from the Bored Ape Yacht Club.

· Whitelisting: Bloomberg reported on Chainanalysis’s finding that “[t]he practice of whitelisting appears to be similar to the preferential treatment of some insiders and investors that has long been practiced in the cryptocurrency world, especially with so-called initial coin offerings before the sales were shut down by regulators”. Citing the Chainanalysis study, Bloomberg also noted that “[u]sers who make the whitelist and later sell their newly-minted NFT gain a profit 75.7% of the time, versus just 20.8% for users who do so without being whitelisted”

· Official Auction Houses: Beeple did not sell his $69 million piece of digital art on some random site on the Internet. He sold it at Christie’s. Christie’s has been around since 1766. It doesn’t get more classic than that.

Issue 10: NFTs are rife with information security issues

Speaking as a CPA/CISA, one of the craziest aspects of NFTs is that the process requires you to grant the entity issuing NFT (or the minter) logical access to your wallet. And what happens if you grant access to the wrong individual, i.e. a hacker? All that crypto will be emptied out.

The other scam that is out there is that people can “airdrop” an NFT into your wallet. And if you click on that? As RAC explained to Rolling Stone, “[e]verything’s programable, so what they do is they make these tokens unsellable. It basically locks you into something and forces you to give them access to your funds, and then they steal your money.”

What RAC is referring to is the programmability that’s baked into the Ethereum blockchain. Consequently, clicking something (even deleting something) could initiate malware that would result in your digital wallet being drained of funds.

Closing thoughts:

So with all these problems, what does the future look like?

It’s really about governance. The unregulated nature of stocks in the 1920s ultimately led to the Great Depression, which brought the Security Exchange Commission into existence and the need for financial audits. Similarly, governance will ultimately need to be implemented to enable true ownership of not just the hash in the NFT but the underlying asset. That is, just like you own a painting, you should have the underlying code that is the actual digital art.

In terms of AML, Know Your Customer (KYC) controls are percolating at NFT marketplaces. Wired reported that:

“A Twinci spokesperson says the platform is implementing something like this at the moment – it is verifying artists to make them stand out from ordinary users. Green-ticked artists have verified their identity in a process similar to how Twitter doles out its blue ticks. People are asked to give their name, a photo of themselves, proof of them creating an artwork as well as a digital portfolio. Twinci cautions its community to re-consider collecting NFTs from non-verified artists.”

But doesn’t this contradict the decentralization that blockchain is supposed to bring?

The challenge with this idea is largely based on the myth of individualism. Society is not simply composed of individuals. Rather, it’s the institutions and collectively shared norms that hold society together. For example, if Canadians did not collectively respect private property then anything you held could be stolen without recourse. But perhaps the greatest illustration of such conventions goes back to how disputes were handled on the blockchain itself. Consider the DAO hack of 2016. The consensus amongst the Ethereum community felt and injustice was done because of the theft of ether (the cryptocurrency used on Ethereum). So they turned to Ethereum’s leader/inventor, Vitalik Buterin, to mutate the immutable. This is why the term “immutable” shouldn’t really be used; tamper-resistant is more accurate.

Consequently, once such myths give way to practical necessities of governance (e.g. SEC-type organizations managing minting, courts opining on digital ownership, ISO standards, etc.); we will be on our way from the current wild west to something safe and stable. Again, this is history repeating itself. The cloud took time for standards to take hold. For example, cloud service providers see the SOC2 audit report on the IT controls as a standard. But it wasn’t always. In the early days of cloud, it was rumored that Eli Lily had to walk away from Amazon because they could not offer the IT controls that they needed (which Amazon denied). Regardless, the security norms took a while to become the status quo. Similarly, this standardization is part of the process to take the NFTs from the Trough of Disillusionment to the Slope of Enlightenment. This is the next phase of Gartner’s Hype Cycle. Only time will tell how players within the industry will coalesce around such standards given that the NFT/blockchain evangelists are still stuck with the idea that society is unnecessary.

Author: Malik Datardina, CPA, CA, CISA. Malik works at Auvenir as a GRC Strategist that is working to transform the engagement experience for accounting firms and their clients. The opinions expressed here do not necessarily represent UWCISA, UW, Auvenir (or its affiliates), CPA Canada or anyone else